China's E-Commerce Innovations and Retail Media: Lessons for Australian Retailers

Introduction: Reflections from My Time in China's Retail Frontier

Having spent nearly five years in China deeply immersed in the rapidly evolving landscape of retail media and e-commerce innovation, I've witnessed firsthand how advanced omni-channel integration, private domain operations, and data-driven retail media strategies have transformed the consumer experience. From pioneering platforms like Alibaba and JD.com to the rise of live streaming commerce and WeChat-driven private communities, China's retail sector is leading the charge in redefining how brands engage, monetize, and nurture their customer relationships.

China's Omni-Channel and Private-Domain E-commerce Ecosystem

China's retail landscape has evolved into a seamless omni-channel ecosystem where online, offline, and social commerce converge. Major retailers and platforms integrate physical stores with digital channels to capture consumers wherever they shop. Shoppers routinely switch between e-commerce apps, social media, and brick-and-mortar stores – in fact, 73% of Chinese consumers use multiple channels during a single shopping journey. Retailers respond with unified experiences: for example, grocery chains offer buy-online-pickup-in-store services and on-demand delivery from local outlets, blending convenience with instant fulfillment.

Equally transformative is China's focus on "private domain" customer engagement – brand-controlled channels like official apps, loyalty programs, and especially WeChat mini-programs and groups. As public platform customer acquisition costs rise amid fierce competition, brands have embraced private-domain operations to drive loyalty and repeat purchases. WeChat, with over 1.3 billion users, is central to this strategy. Lightweight WeChat mini-programs (sub-apps within WeChat) enable brands to interact with customers directly without requiring a separate app download. By 2023, WeChat mini-program users reached 900 million, underscoring how entrenched this channel has become.

Membership and loyalty programs tie into both omni-channel and private traffic strategies. Chinese consumers are famously enthusiastic about memberships – from supermarket apps to luxury malls, it's common to be prompted to "join as a member" at the first interaction. This "membership-first, purchase-later" approach flips the traditional funnel: by enrolling customers early (often with small incentives or gamified sign-ups), businesses rapidly build a database of first-party data and a direct line to customers. Many leading retailers have even launched paid membership tiers to deepen engagement. Alibaba's 88VIP, for example, offers annual members exclusive discounts and perks across Alibaba's online marketplaces and services, cultivating high-value repeat shoppers.

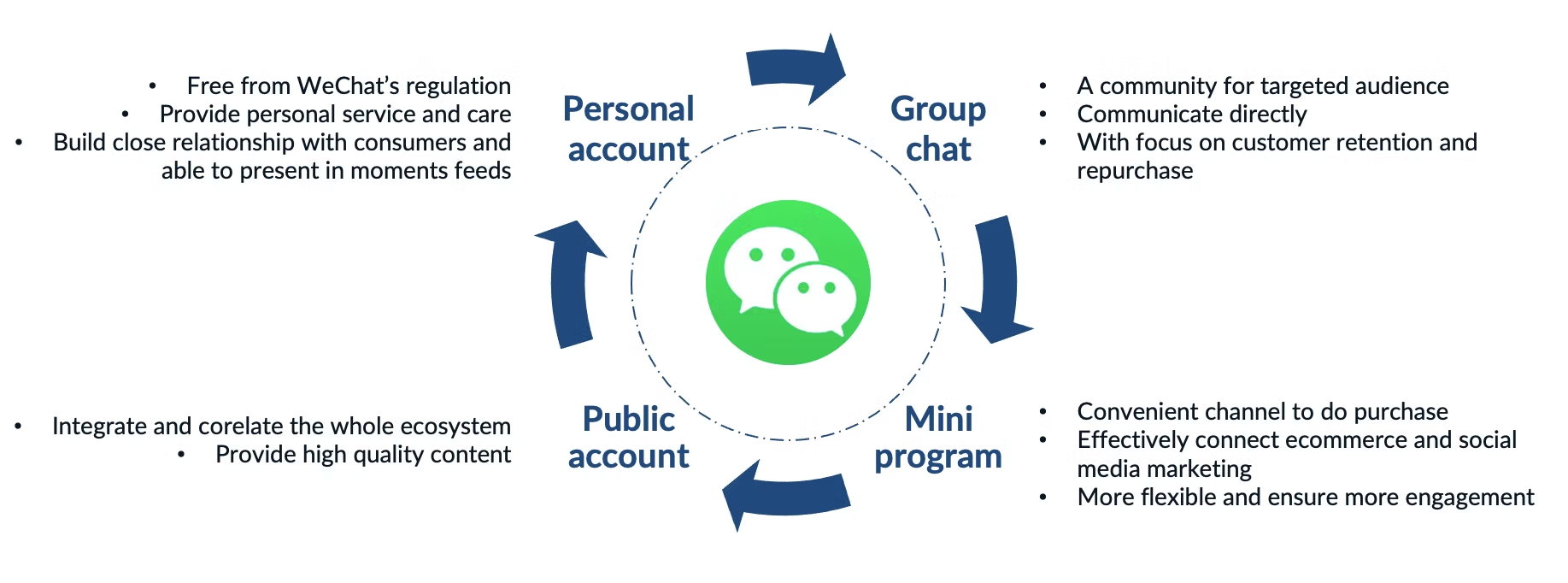

WeChat Mini-Programs, Live Commerce and Private Traffic in Action

Swisse, an Australian health brand, uses a WeChat mini-program with interactive features – a members center, health quizzes, and referral incentives – to engage Chinese consumers in its private domain. Through its WeChat mini-program and official account, Swisse built a highly engaged community as the core of its China business. New followers receive an automated welcome message guiding them to join the "Swisse SI Family" loyalty club and access features like nutrition consultations and VIP customer service.

Beyond brand-operated channels, China's live streaming commerce boom has redefined online shopping. In the past five years, live commerce – real-time interactive video sales – grew from novelty to a 5 trillion CNY (≈A$1 trillion) market as of 2023. Live-streaming now accounts for roughly 32% of all Chinese e-commerce GMV, with hundreds of millions tuning in to watch product demos, flash deals, and influencer reviews. Top streamers (known as KOLs) can sell millions in minutes by blending entertainment with shopping.

Importantly, these private domain and content-driven tactics feed a larger strategy: traffic monetization and retail media. Every customer in a brand's private network can be re-engaged at low cost, and every follower or stream viewer is a potential target for upselling or cross-selling. Home-grown cosmetics brand Perfect Diary famously built its success on private traffic, cultivating loyalty groups on WeChat – an effort that drove an estimated 15% of the brand's sales.

Data-Driven Retail Media and Precision Marketing in China

Underpinning China's e-commerce ecosystem is a sophisticated use of first-party data and precision marketing. Every omni-channel interaction – whether a scan of a QR code in a store, a click on a mini-program, or a product added to a livestream cart – feeds into data platforms. Leading retailers aggregate these signals to build 360° customer profiles for targeting and personalization. For example, Alibaba's marketing technology leverages data from its e-commerce (Taobao/Tmall), payments (Alipay), logistics and social apps to let brands target ads to highly specific audience segments.

China's early adoption of retail media networks is evident in sheer spending numbers. As of 2019, China made up 66% of global retail media ad spending – far surpassing the US's ~24% share. By 2022, retail media in China was estimated to reach US$55.6 billion, an astonishing 40%+ of all digital ad spend in the country. These platforms have effectively become media owners: they monetize their e-commerce "shelf space" and data insights to help brands target shoppers at the point of purchase.

Implications for the Australian Retail Sector

Australia's retail sector, while different in scale, is rapidly moving toward some of the same models now commonplace in China – especially in the realm of retail media. Major Australian retailers have launched their own media businesses to monetize shopper data and attention. For instance, Woolworths Group's Cartology and Coles Group's Coles 360 offer suppliers advertising placements across supermarkets' digital and physical assets, powered by loyalty card insights.

Learning from China: Consumer Engagement Tactics

- Deep Omni-Channel Engagement: Australian retailers do offer omni-channel services (click-and-collect, online returns, etc.), but Chinese retailers go further in blurring channels. For example, experiential flagships in China use AR, interactive screens, and app integrations to make store visits as data-rich as online visits.

- Private Domain and Community Building: The concept of cultivating a direct audience "owned" by the brand is something Australian brands can embrace more. Outside of email lists and basic loyalty apps, few Australian retailers run community content platforms.

- Live Commerce and Social Selling: While live shopping is still niche in Australia, interest is growing, especially among younger consumers. In 2023, over half of Australian social media users were aware of live commerce and about 31% had participated in a live shopping event.

- Paid Membership and Loyalty Perks: Australian shoppers are used to free loyalty programs; paid retail memberships are less common. Chinese retailers have shown that consumers will pay for memberships if the value is clear – 88VIP's success is evidence of that.

Data Strategy and Media Monetization

- Leverage First-Party Data for Personalization: Most Australian retail media networks already use purchase history for targeting. The next step is more real-time and predictive personalization.

- Closed-Loop Measurement: Australian retailers should highlight their ability to tie ads to sales outcomes using loyalty data – a strength over other media.

- Expand Retail Media Inventory: One limitation in Australia is fewer digital super-app environments compared to China. But retailers can think creatively to broaden ad inventory.

- Collaborate and Learn: Australian retailers and brands should keep a close eye on Chinese market trends for inspiration.

Conclusion

China's e-commerce ecosystem showcases how omni-channel integration, private domain engagement, and data-driven retail media can create a powerful growth engine. By marrying online and offline channels, cultivating owned customer communities, and relentlessly monetizing traffic through precision ads and content, Chinese retailers have built a retail media juggernaut that is now a core part of their business model.

For the Australian retail sector, the rise of retail media networks and the increasing value placed on first-party data signal a similar transformation underway. Australian retailers and FMCG brands stand to gain by borrowing the best of Chinese innovation: investing in richer consumer engagement platforms, embracing new formats like live commerce and interactive content, and using their data troves to deliver personalized, high-ROI marketing for themselves and their partners.

In summary, China offers a glimpse of a retail future where the lines between shopping, media, and digital services blur. Australian retailers can accelerate their retail media journey by adapting these proven strategies in consumer engagement and data use. The playbook is there; it's now about execution in the Australian context.

References

- China Trading Desk. (2024). China Private Domain Traffic Marketing. Retrieved March 21, 2025.